Naples FL Closing Costs — What Buyers and Sellers Actually Pay in 2026

Closing costs in Naples are predictable once you know what is inside them. This guide breaks down every line item for buyers and sellers — what is fixed, what is negotiable, and where people consistently overpay.

What Closing Costs Actually Are

Closing costs are the fees and prepaid items required to transfer a property, establish title, and set up any associated financing. They are collected at the closing table — usually handled in Naples by a title company — and they appear in the Closing Disclosure for financed buyers and the settlement statement for sellers.

In Naples, closing costs surprise buyers and sellers from the Northeast because Florida's cost structure is different from New York, New Jersey, or Connecticut in several specific ways. The documentary stamp tax, the owner's title insurance custom, and the property tax proration structure are all Florida-specific and unfamiliar to most out-of-state buyers. This guide covers all of them.

Ballpark ranges for 2026 Naples transactions: Buyers with a mortgage typically pay 2–5% of the purchase price in closing costs. Cash buyers typically pay 1–3%. Sellers, excluding mortgage payoff, typically pay 3–8% depending on commission structure and concessions negotiated.

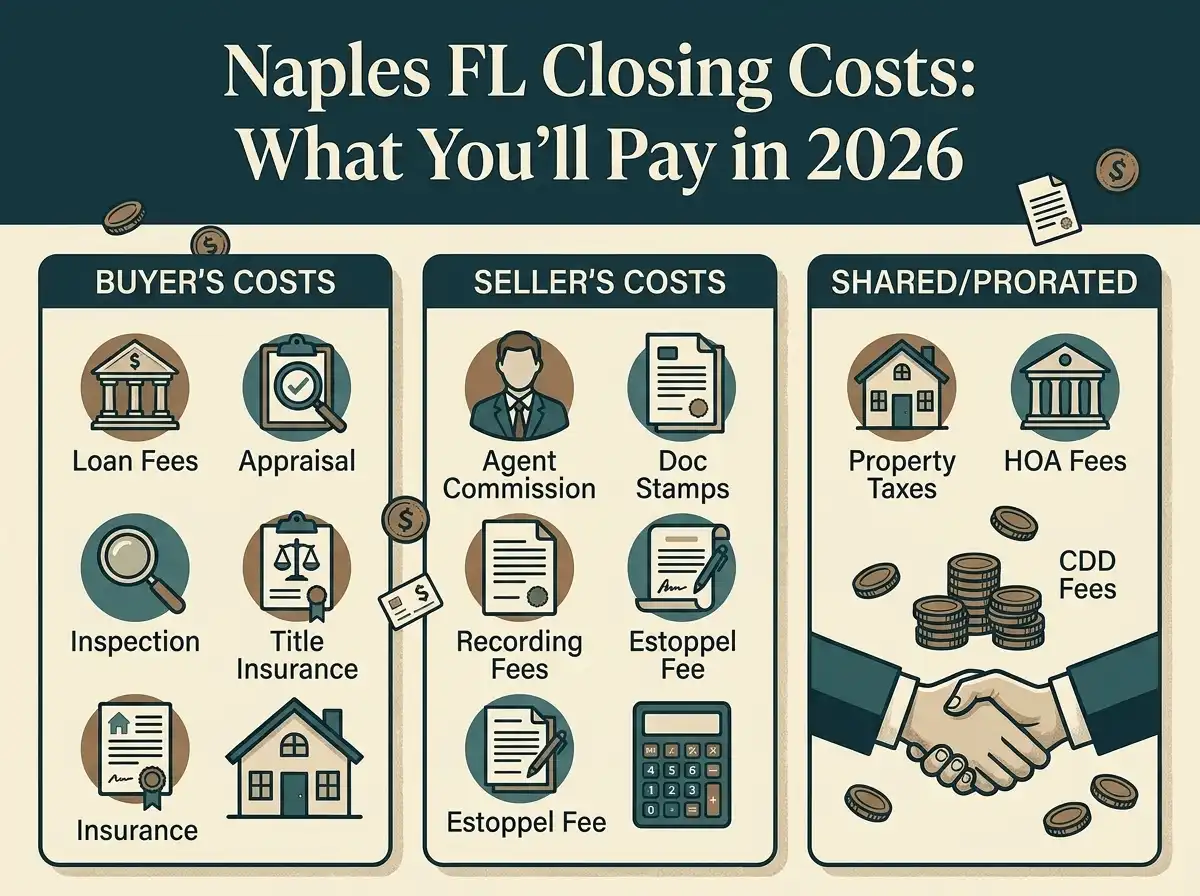

Buyer Closing Costs — Every Line Item

Buyer costs fall into four categories: loan-related fees, title and settlement fees, government taxes and recording, and prepaids and escrows. Here is what each category contains and what to budget for each on a Naples purchase.

| Cost Category | What's Included | Typical Range on $750K |

|---|---|---|

| Loan / lender fees | Origination, appraisal, credit report, flood cert, underwriting, processing. Compare total cost across lenders — not just the origination label. | $2,000–$6,000 |

| Title and settlement | Title search, closing/settlement fee, lender's title insurance policy (required with a loan), owner's title insurance (strongly recommended even for cash buyers). | $2,500–$5,500 |

| Recording and government taxes | Recording fees for deed and mortgage. Mortgage doc stamp tax and intangible tax — Florida-specific charges based on loan amount, not purchase price. | $1,500–$4,500 |

| Prepaids and escrows | First year homeowners insurance premium, property tax escrow deposit, prepaid interest (closing date to month end), flood insurance if required or elected, HOA dues escrow if required by lender. | $5,000–$18,000 |

| Inspections (pre-closing) | General inspection, 4-point inspection (often required for insurance on older homes), wind mitigation, roof inspection if needed. Paid before closing, not on settlement statement. | $500–$1,500 |

| Total estimate — financed buyer | — | $12,000–$36,000 |

| Total estimate — cash buyer | Title, recording, inspections. No loan fees, no mortgage taxes, no escrow deposits. | $4,000–$9,000 |

Title Insurance in Collier County — Who Pays What

Florida is a title insurance state, meaning both a lender's policy (required with any mortgage) and an owner's policy (which protects the buyer against title defects discovered after closing) are standard in every transaction. The cost is based on the purchase price and is set by state-filed rates — the premium does not vary between title companies.

In Collier County, there is a local custom: the seller typically pays for the owner's title insurance policy. This is different from some other Florida counties and from most northeastern states where the buyer pays. It is also negotiable — in a buyers' market or in distressed sale situations, the buyer may end up paying it. Do not assume the custom will hold in every deal. Verify in the contract.

For buyers paying cash who think they can skip the owner's policy to save money: the premium is a one-time cost that protects you against title defects that could surface years after closing. On a $750,000 Naples home, the owner's title policy costs approximately $3,500–$4,500. The exposure it covers is the full purchase price. It is not optional in any practical sense.

Property Tax Prorations — The Florida Arrears System

Florida property taxes are paid in arrears — the 2026 tax bill is paid in November 2026 for the full calendar year 2026. This creates a proration at every closing where the seller owes the buyer a credit for the days of the year the seller owned the property, even though the tax bill has not yet been issued.

The proration is calculated using the prior year's tax bill divided by 365, multiplied by the seller's days of ownership in the current year. The earlier in the year you close, the smaller the seller's credit. The later in the year, the larger. On a $750,000 Naples home with a $7,500 annual tax bill, a March closing produces approximately a $1,500 credit from seller to buyer. An October closing produces approximately $5,600.

This is not a fee. It is a cash flow shift between buyer and seller at closing. But it affects the seller's net proceeds and the buyer's cash-to-close, so it needs to be in both calculations from the beginning.

Seller Closing Costs — Every Line Item

Sellers pay fewer line items than buyers but the amounts are larger, because the documentary stamp tax on the deed and the listing commission are both based on the full sale price — not the loan amount or a fixed fee.

| Cost Category | What's Included | Typical Range on $750K Sale |

|---|---|---|

| Listing commission — Realty of Naples FL | Our listing fee is 1% of the sale price. Full-service marketing, negotiation, and closing support included. | $7,500 (1%) |

| Doc stamp tax on deed | Florida charges $0.70 per $100 of sale price on deed transfer. Seller-paid, non-negotiable state tax. | $5,250 |

| Owner's title insurance | Seller-paid by Collier County custom. One-time premium based on sale price. | ~$3,800 |

| Title/settlement fee | Closing agent or title company administrative fee. | ~$600 |

| HOA/condo estoppel | Required document from association confirming dues current and no pending assessments. Fee charged by management company. | $100–$500 |

| Municipal lien search | Confirms no open permits, code violations, or city liens against the property. | ~$200 |

| Property tax proration | Credit to buyer for seller's portion of current year taxes not yet billed. Varies by close date. | Varies |

| Mortgage payoff | Outstanding loan balance plus per diem interest to closing date. Request a 10-day payoff statement from your lender before listing. | Your balance |

| Total estimate (excl. payoff) | — | ~$18,000–$24,000 |

Three Scenarios — What Both Sides Actually Pay

These are planning estimates using Collier County customs, our 1% listing fee, and standard 2026 market conditions. Your actual figures depend on loan type, close date, HOA structure, and negotiated terms.

| Scenario | Buyer Closing Costs | Seller Closing Costs (excl. payoff) | Commission to Seller |

|---|---|---|---|

| $500,000 — financed buyer | ~$11,000–$22,000 | ~$14,000–$17,000 | $5,000 (1%) |

| $750,000 — financed buyer | ~$16,000–$34,000 | ~$18,000–$24,000 | $7,500 (1%) |

| $1,000,000 — cash buyer | ~$5,000–$10,000 | ~$22,000–$30,000 | $10,000 (1%) |

What You Can Shop — and What You Cannot

Not all closing costs are equal. Some are fixed state taxes with no negotiation possible. Others vary significantly depending on who you choose and when you act.

- Shop aggressively: Your lender — total loan cost comparison matters far more than origination fee labels. Homeowners insurance — get quotes early, before the 30-day inspection window closes. Inspectors — quality and price vary.

- Sometimes negotiable: Title company selection — depends on contract terms and who has the right to choose. Some seller title fees can be negotiated in the contract.

- Fixed — not worth fighting: Florida documentary stamp taxes (buyer and seller), recording fees, intangible tax on the mortgage. HOA estoppel fees — the association sets them; you pay or you don't close.

Naples-Specific Items That Catch Out-of-State Buyers

The 4-point inspection. Insurance carriers in Florida frequently require a 4-point inspection on homes over 10–15 years old before issuing a policy. This covers roof, electrical, plumbing, and HVAC. If any of the four systems fails, you may face a coverage denial or a significant premium increase. Schedule this inspection early — not as an afterthought in the final week.

Flood insurance timing. Flood insurance can be required by your lender based on FEMA flood zone mapping, or it may be optional but advisable depending on the property. Standard homeowners insurance does not cover flood damage. In Naples, where storm surge is a realistic risk in certain areas, flood insurance cost needs to be in your monthly payment estimate before you make an offer — not discovered at closing.

Condo closing extras. Naples condo transactions often involve additional HOA application fees, board approval timelines that affect your closing date, required condo questionnaires for financing, and updated building insurance certifications. Budget 2–4 extra weeks for condo closing timelines and $200–$800 in additional association-related fees beyond the standard estoppel.

How to Reduce Closing Costs Without Doing Anything Unusual

For buyers, the biggest lever is lender comparison. Request Loan Estimates from at least two lenders for the same loan amount, same down payment, and same rate lock period. Compare total costs — Section A through Section C of the Loan Estimate — not just the interest rate. Lenders package fees differently, and the variation on a $600,000 loan can easily be $3,000–$5,000 between institutions.

For sellers, the most impactful cost reduction is the listing commission. Our 1% listing fee is fixed and transparent. On a $750,000 sale that is $7,500. On a $1,000,000 sale that is $10,000. Those are dollars that stay in your net proceeds and fund your next purchase, your move, or your retirement — not a percentage that disappears into a transaction.

Both buyers and sellers benefit from acting early on insurance. Homeowners insurance quotes in Naples should happen in the first week of the contract period — not the last. Carriers and pricing can vary dramatically based on roof age, construction type, wind mitigation credits, and flood zone. A bad insurance outcome discovered in the final week creates closings delays and sometimes deal failures.

Enter your sale price and mortgage balance. See your full walkaway after doc stamps, title fees, and our 1% listing commission.

Run Your Net SheetScott walks buyers and sellers through a complete closing cost estimate before anyone signs anything. No surprises at the table.

Talk to Scott