1031 Exchange in SWFL — Nine Timing Traps to Avoid

The 1031 exchange clock does not care about your travel schedule, your tenant situation, or your insurance delays. This guide covers the nine ways SWFL investors lose their exchange — and what to do instead.

This guide is a practical overview for investors considering a 1031 exchange in Southwest Florida. It is not tax or legal advice. Work with a qualified intermediary and a CPA experienced in 1031 exchanges before making any decisions based on this information.

The Core Mechanics — Before We Get to the Traps

A 1031 exchange allows an investor to defer capital gains tax on the sale of investment property by reinvesting the proceeds into a like-kind replacement property. The tax is deferred — not eliminated — meaning it carries forward until a future taxable sale. The mechanism is straightforward. The execution is where investors consistently lose ground, almost always because of timing.

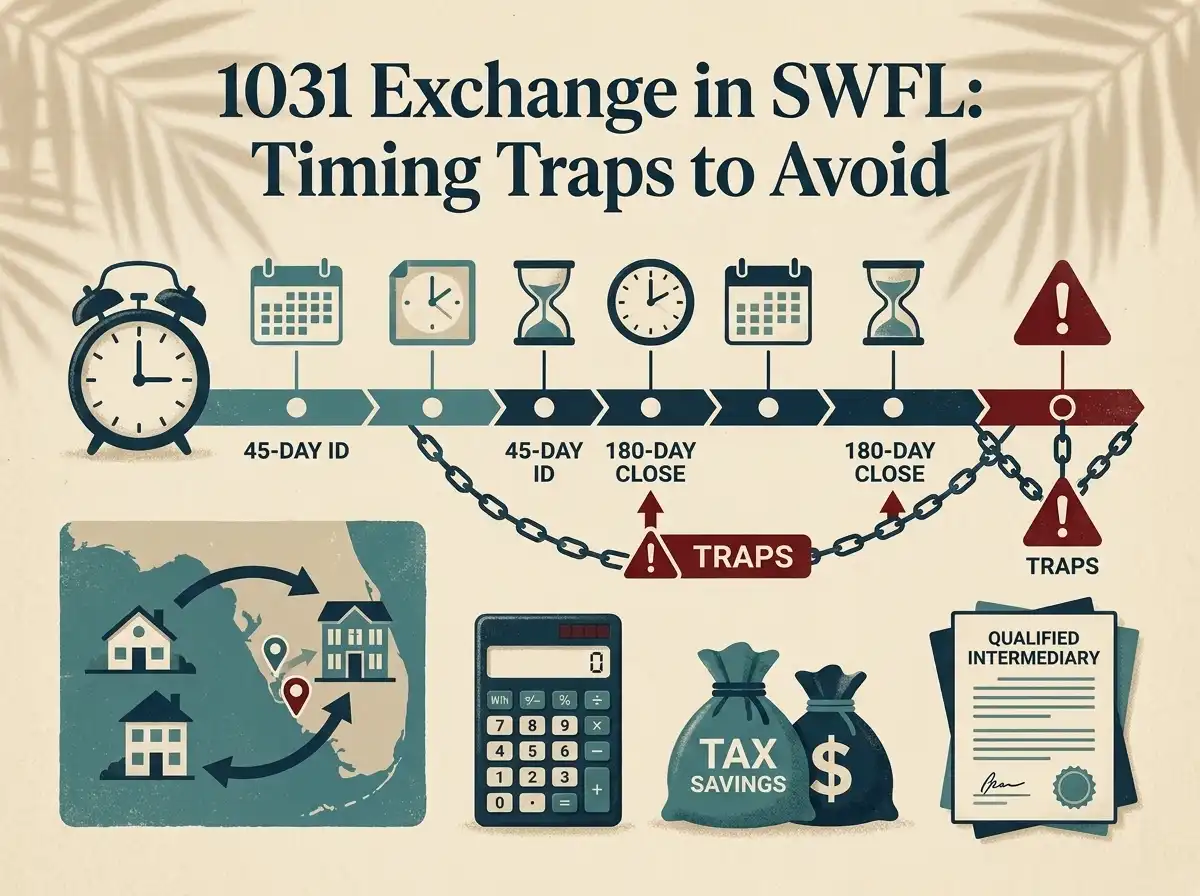

| Deadline | What It Requires | When the Clock Starts | What Kills It |

|---|---|---|---|

| Day 45 — Identification | Written identification of replacement property delivered to your Qualified Intermediary. Must be signed, unambiguous, and describe the property specifically. | The day the relinquished property closes — not when you list, not when you accept an offer. | Missing the deadline by a single day. Vague identification. No backup properties identified. Delivering to the wrong party. |

| Day 180 — Close | Closing on identified replacement property. Title transfers and proceeds are deployed from QI. | Same day as identification clock — day of relinquished property closing. | Financing delays. Appraisal problems. Condo doc issues. Insurance bind failures. Title problems. Missing the tax return due date if it falls before day 180. |

| Tax return due date | Exchange period ends on the earlier of day 180 OR the due date of your tax return for the year of the sale — unless you file an extension. | Applicable if you close the relinquished property late in the calendar year. | Not filing an extension when the tax return due date shortens your 180-day window. |

Trap 1 — Waiting to Engage a Qualified Intermediary Until After You Are Under Contract

The Qualified Intermediary (QI) is the independent party who holds your exchange funds and manages the paperwork that keeps the transaction compliant. The critical rule: you cannot have actual or constructive receipt of the sale proceeds. If the closing proceeds are wired to you — even for a single day, even "accidentally" — the IRS may treat that as a taxable sale and the exchange is over.

This means the QI must be engaged and the exchange cooperation language must appear in the purchase contract before closing. You cannot set up a 1031 exchange retroactively after you have already closed a sale. The sequence is: engage QI → get exchange language into the contract → close → QI receives funds. Any deviation from this sequence introduces risk that can be fatal to the exchange.

In practice: if you are considering a 1031 exchange when you list your SWFL investment property, engage the QI before you accept an offer. The cost is minimal and the downside of waiting is potentially the entire tax deferral.

Trap 2 — Treating the 45-Day Window as Generous in the SWFL Market

In a market with deep, liquid inventory and predictable condo documentation, 45 days can feel like adequate time to identify a replacement property. Southwest Florida is not always that market. Inventory in specific neighborhoods and product categories is uneven. Insurance review cycles add time. HOA rental rules, condo reserve studies, and special assessment disclosures require research before you can confidently identify a property. And the 45-day clock continues running while you do all of this.

The pattern that kills exchanges: buyer spends weeks 1 and 2 watching the market, tours in week 3, finds something promising in week 4, and then discovers on day 38 that the condo building has financing issues or rental restrictions that eliminate it from consideration. Now they have 7 days to identify something else, tour it, verify it, and submit the identification letter.

The solution is to start your replacement property search before you close the relinquished property. You are not committing to a purchase. You are building a shortlist of realistic candidates so that when your clock starts, you are not starting from zero. Talk to your agent about the replacement criteria before you list — not after you close.

Trap 3 — Misunderstanding Identification Rules and the Backup Problem

The identification notice must be written, signed, delivered to the correct party (usually your QI), and provide an unambiguous description of the replacement property — typically the legal address. The identification must be delivered by day 45, not postmarked by day 45, not drafted by day 45. Delivered and received.

Identification mistakes that commonly blow exchanges:

- Vague identification — "any unit in Building X" is not sufficient. The specific unit must be identified.

- Identifying a property that is already under contract with another buyer, meaning you cannot actually close on it.

- Failing to identify backup properties because the primary candidate feels certain — and then losing the primary during due diligence after day 45.

- Identifying only one property without understanding that the 3-property rule allows up to three identifications with no value limit, providing meaningful protection against losing your primary option.

The 3-property rule is the standard approach for most SWFL exchanges: identify up to three properties, close on at least one. The emotional resistance to identifying backups is understandable — it feels like admitting uncertainty. But in a market where inspections, condo docs, and financing can derail a deal between offer acceptance and closing, backup identification is not pessimism. It is competence.

Trap 4 — Underestimating Condo Document Review Time in SWFL

A significant portion of SWFL investment property exchanges involve a condo as either the relinquished property, the replacement property, or both. Condo document review is not a formality in Florida's current environment. Post-Surfside legislation has created new reserve requirements, Milestone Inspection obligations, and Structural Integrity Reserve Study requirements that directly affect condo building financials, special assessment risk, and lender project approval status.

Getting answers to basic condo due diligence questions takes time. Reserve funding levels, pending or approved special assessments, Milestone Inspection completion status, insurance coverage adequacy, litigation disclosure, and rental restriction details all require document review and sometimes direct communication with the management company. In well-managed buildings, this process takes days. In less organized associations, it can take weeks.

For 1031 exchange buyers, slow condo document response is a timing risk that needs to be factored into replacement property selection. If you are considering a condo replacement, ask your agent before you identify: how quickly does this building's management company typically respond to condo questionnaires? Is the building Fannie Mae approved? Are there any known open assessment discussions? If those answers are slow or uncertain, prioritize it in your identification timeline accordingly.

Trap 5 — Assuming 180 Days Is Enough Time for Financing to Close

The 180-day deadline feels comfortable until it isn't. SWFL financing delays that consume the clock in ways investors do not anticipate:

- Appraisal delays: in submarkets with thin comparable sales — waterfront properties, unique floor plans, luxury condos — appraisals take longer and have a higher rate of revision requests.

- Condo project approval: Fannie Mae and Freddie Mac project approval requires documentation from the HOA that can take weeks to compile, particularly for buildings that have not recently gone through the approval process.

- Insurance binding issues: if the replacement property has an aging roof, a flagged electrical system, or a flood zone designation that triggers specific underwriting requirements, insurance can delay closing by days or weeks.

- DSCR and commercial lending: investors using debt service coverage ratio loans or commercial financing for the replacement property should expect longer processing timelines than conventional residential financing.

- Self-employed borrower documentation: lenders requiring 2 years of tax returns, business financial statements, and CPA letters can take longer than W-2 borrowers even when the file is well-organized.

The fix is to start the financing conversation before you close the relinquished property. You are not committing. You are eliminating uncertainty. If you know your loan type, your lender's timeline, and your likely replacement property category before day one, you can build a realistic closing target into your 180-day window rather than discovering a 45-day financing timeline on day 135.

Trap 6 — Not Accounting for the Tax Return Due Date

The 180-day exchange period ends on the earlier of day 180 or the due date of your federal tax return for the year in which the relinquished property closed — unless you file an extension. This creates a specific risk for late-year closings.

If your relinquished property closes on November 15, your 180-day window extends to May 14 of the following year. But if your tax return is due April 15 and you do not file an extension, your effective exchange deadline is April 15 — 29 days shorter than your 180-day window. Many investors do not discover this until they are working backward from a planned closing date and realize the timeline does not work the way they thought.

The fix is simple: if your relinquished property closes in the fourth quarter, bring your CPA into the timeline conversation before day one and confirm whether an extension is appropriate. An extension to file is not an extension to pay — consult your CPA on the implications — but it does preserve your full 180-day exchange window.

Trap 7 — Planning an Improvement Exchange Without Accounting for SWFL Construction Timelines

An improvement exchange (sometimes called a build-to-suit or construction exchange) allows the replacement property to be improved using exchange funds, with the improved value counting toward the exchange requirements — provided the improvements are completed within the 180-day window. The appeal is that an investor can acquire a lower-priced replacement property and use exchange funds for renovations to reach the required reinvestment level.

In Southwest Florida, construction timelines are not reliable planning inputs. Permit processing, contractor availability, material supply, and weather delays — particularly during hurricane season — can extend construction timelines significantly beyond initial estimates. An improvement exchange that assumes 90 days of construction in a market where permit processing alone can take 30–60 days is an exchange that is likely to fail.

If an improvement exchange is part of your plan, the contractor must be identified and mobilized, permits applied for, and a realistic timeline established before the exchange clock starts — not in month three of the 180-day window. This requires specific expertise and coordination that not all real estate professionals routinely handle. Engage professionals who have managed improvement exchanges in Florida specifically.

Trap 8 — Selling Without a Realistic Replacement Strategy in Place

The most emotionally driven timing trap: selling because you received a strong offer, because your tenant left, because you are ready to exit an HOA situation, or because the timing felt right — without having a realistic replacement strategy identified before you close.

Shopping for a replacement property under a 45-day identification deadline, in a market you may not know well, with limited inventory in your target product category, while simultaneously managing closing logistics on the relinquished property and coordinating with a QI — is a recipe for poor decisions and failed exchanges. The deals investors accept under deadline pressure are rarely the deals they would have selected with more time.

A more controlled approach: before you list the relinquished property, identify your target replacement criteria — product type, geography, price range, investment thesis. Run a preliminary search. Verify that realistic replacement candidates exist in your target market at your target price. Only then time the listing and close to coincide with the availability of properties you have already pre-qualified as candidates. You are not committed to buying. You are ensuring you have something to buy before the clock starts.

Trap 9 — Assuming Your Agent, QI, Lender, and Title Company Are Automatically Coordinated

A 1031 exchange is a coordination project involving at minimum four parties: your real estate agent, your Qualified Intermediary, your lender (if financing), and the title company. Each party has a specific role and a specific set of timing dependencies. Exchanges fail not because any single party made a large error, but because no one owned the coordination across all parties and timing slipped in the gaps.

The coordination items that need explicit ownership:

- Exchange cooperation language in the relinquished property sale contract — drafted by the QI, confirmed by the agent before signing

- Wire instructions for QI receipt of sale proceeds — confirmed with title company before closing, not at closing

- Day 45 identification letter format and delivery requirements — confirmed with QI, drafted and delivered with a buffer day or two

- Replacement property contract exchange cooperation language — confirmed with QI before signing

- Replacement property closing scheduled with QI funds availability — confirmed with QI and title company jointly

- Financing timeline mapped against the 180-day window — confirmed with lender before identification is submitted

Ask for a written timeline checklist from your QI at the beginning of the exchange and circulate it to all parties. Make everyone work from the same dates. This single action eliminates the majority of coordination failures that derail exchanges in their final weeks.

The Complete SWFL 1031 Exchange Timing Checklist

- QI engaged before the relinquished property listing goes live — not after you accept an offer

- Exchange cooperation language confirmed in the sale contract before you sign

- Replacement property search started before closing — shortlist of candidates ready on day one

- Tax return due date reviewed with CPA — extension filed if needed to protect the full 180 days

- Identification of up to three replacement properties prepared with buffer before day 45

- Backup properties identified — do not rely on a single candidate

- Condo document timelines verified for any condo replacement candidates

- Financing conversation with lender started before the relinquished property closes

- Insurance binding timeline confirmed for the replacement property before identification

- Wire instructions from QI to title company confirmed in writing before the relinquished property closes

- Replacement property closing target set with buffer before day 180 — not on day 180

- All parties working from the same written timeline checklist from day one

What to buy in Naples, where to buy it, what it costs to own, and how to evaluate a SWFL investment property for rental income.

Read the GuideScott coordinates 1031-friendly listing timelines with title and your QI. Talk before you list — not after you close. Free, no obligation.

Talk to Scott