NY/NJ Taxes vs Florida — What Actually Changes When You Move to Naples

"No state income tax" is true and incomplete. The full picture includes residency rules, property tax mechanics, retirement income treatment, and the traps that catch people who don't fully cut ties with New York. This guide covers all of it.

This guide is a practical overview for people planning a move from NY or NJ to Florida. It is not tax or legal advice. Consult a CPA familiar with multi-state residency issues before making decisions based on any of the information here.

The Complete Tax Picture — What Changes and What Stays

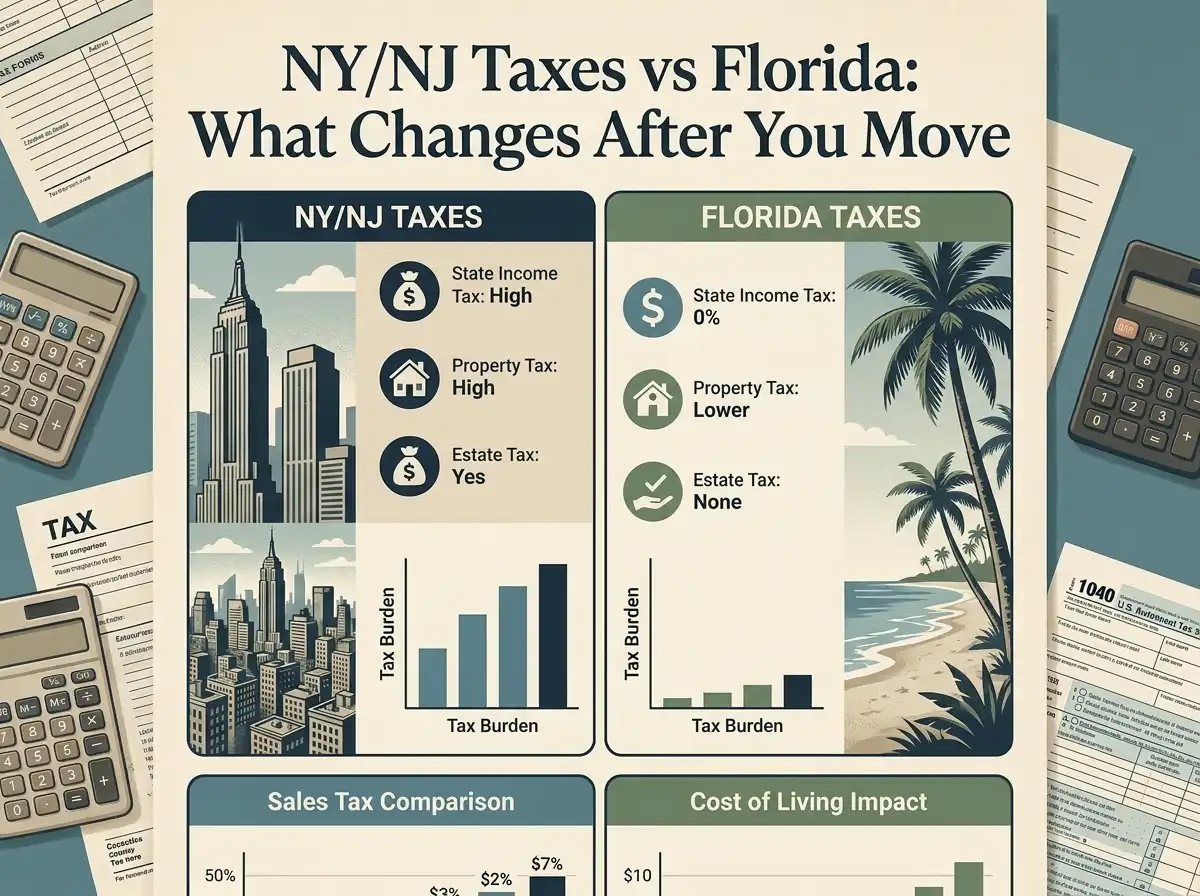

The "no state income tax" headline is accurate and real. But it is one line in a longer story. Moving from New York or New Jersey to Florida changes the entire structure of your tax life — some taxes disappear, some get smaller, some shift from income-based to consumption-based, and a few new considerations appear that did not exist in your prior state. The net result for most households moving from high-income positions in NY/NJ is significantly positive. But the result is not automatic and not uniform — it depends on how completely you execute the move and how your income is structured.

| Tax Category | New York | New Jersey | Florida |

|---|---|---|---|

| State income tax | Yes — up to 10.9% (NYC adds more) | Yes — up to 10.75% | None |

| Social Security income | Partially exempt | Exempt | Not taxed — no income tax |

| Pension / retirement income | Partial exemptions vary | Partial exemptions vary | Not taxed — no income tax |

| 401(k) / IRA withdrawals | Taxed at state rate | Taxed at state rate | Not taxed — no income tax |

| Capital gains | Taxed as ordinary income | Taxed as ordinary income | Not taxed — no income tax |

| Property tax | High — especially with school tax | Among highest in US | Varies — homestead exemption available |

| Sales tax | 4% state + local (NYC 8.875%) | 6.625% | 6% state + county surtax (Collier Co. 7%) |

| Estate tax | Yes — state estate tax applies | No estate tax (eliminated 2018); inheritance tax in some situations | None |

| Inheritance tax | None | Yes — applies to non-spouse, non-child beneficiaries | None |

The Residency Rules — Where the Move Can Go Wrong

The most consequential and most misunderstood aspect of moving from New York to Florida is New York's residency enforcement. New York does not simply accept that you have moved. It requires you to prove it. And it has two separate legal frameworks for determining whether your move was real.

Domicile is your true permanent home — the place you intend to return to, where your life is anchored. Changing domicile from New York to Florida requires demonstrating that Florida is now that place, and that New York is not. This is a facts-and-circumstances determination that the New York Department of Taxation and Finance can challenge through an audit.

Statutory residency is the second and more mechanical rule. Even if your domicile has changed to Florida, New York can still treat you as a New York resident for tax purposes if you meet both conditions: you maintain a "permanent place of abode" in New York (which can include a home you own, rent, or have continuous access to — including a family member's residence in some cases), and you spend 183 days or more in New York during the calendar year. A day in New York counts even if you arrive late at night or leave early in the morning.

Establishing Florida Residency — What Actually Counts

A clean Florida residency establishment is both a legal exercise and a documentation exercise. The goal is to build a paper trail that demonstrates Florida is your true home — not just a tax-advantaged address — and that your ties to New York or New Jersey have been substantively reduced. Audit triggers most commonly include high-income taxpayers who maintain property in New York and whose day counts are close to the 183-day threshold.

The steps that carry the most weight in a residency challenge:

- Florida driver's license: surrender your NY/NJ license and obtain a Florida license. This is one of the first items auditors review.

- Florida voter registration: register to vote in Florida and update registration if you previously voted in NY/NJ.

- Florida homestead exemption: if you purchase a primary residence in Florida, apply for homestead. This is a strong domicile signal — you cannot claim homestead on a vacation property.

- Bank, investment, and insurance accounts: update primary mailing address to Florida on all financial accounts.

- Medical and professional relationships: establish Florida primary care physician, dentist, attorney, and CPA. These relationships are evidence of where your life is actually centered.

- Personal property: move meaningful personal property to Florida — family documents, heirlooms, art, items of sentimental or financial significance. Courts have looked at this in domicile cases.

- Day log: maintain a contemporaneous record of where you sleep each night, from the effective date of your move. If audited, this log is your primary evidence. Do not reconstruct it from memory later.

Property Taxes — Why Florida Is More Complicated Than It Looks

Florida has property taxes. In some Collier County locations, effective property tax rates are not dramatically lower than comparable northeastern markets — particularly for non-homestead properties or properties purchased at current market values. What makes Florida property taxes potentially favorable over time is not the rate, but two specific structural features: the Homestead Exemption and the Save Our Homes cap.

The Homestead Exemption reduces the taxable assessed value of your primary residence by $25,000 applied to all taxes, plus an additional $25,000 applied to non-school taxes. For a home assessed at $500,000, this can reduce the taxable value to $450,000 for most purposes. To qualify, the property must be your Florida primary residence as of January 1 of the tax year, and you must apply by March 1 of that year.

The Save Our Homes cap limits the annual increase in assessed value for homestead properties to the lesser of 3% or the change in the Consumer Price Index. In a market where property values increase 10–15% in a single year — as Naples has experienced — this cap means long-term homestead owners pay taxes on assessed values significantly below market value. A neighbor who purchased the same year you did might have the same assessed value. A neighbor who purchased ten years earlier may have an assessed value 40–50% below market, and property taxes to match.

The practical implication: when you buy in Naples, your initial property tax bill reflects the full purchase price. The savings accumulate over time as the cap protects your assessed value from market appreciation. This is a reason to buy and establish homestead sooner rather than later if Naples is your intended long-term home.

Retirement Income — Where Florida's Advantage Is Most Clear

For retirees or those approaching retirement, Florida's income tax treatment of retirement distributions is among the most significant financial benefits of the move. Because Florida has no state income tax, all of the following income sources arrive without state-level taxation:

- Social Security benefits — fully untaxed at the state level

- Traditional pension distributions from public and private plans

- Required Minimum Distributions from traditional IRAs and 401(k) accounts

- Roth IRA distributions (already federal-tax-free; also state-tax-free in Florida)

- Annuity income

In New York, pension income from private employers and IRA/401(k) distributions are generally taxed at the state rate — up to 10.9% for high earners. In New Jersey, retirement income treatment is more favorable than New York but still includes state taxation above certain thresholds. The federal tax treatment of retirement income does not change with your state of residence — Florida does not affect what you owe the IRS. But the state-level elimination is real and for many retiring households represents a meaningful annual savings.

Capital Gains and Liquidity Events — Timing Matters

Capital gains on investment sales, business sales, and real estate sales are taxed by New York as ordinary income — the same rate as wages, up to 10.9% for high earners plus New York City tax if applicable. In New Jersey, capital gains are also taxed at ordinary income rates up to 10.75%. Florida has no capital gains tax at the state level.

This creates a planning opportunity for anyone approaching a large liquidity event — selling a business, selling appreciated stock, liquidating a real estate portfolio, or receiving a large deferred compensation payout. Executing that event after establishing Florida residency and after ensuring New York statutory residency rules do not apply to you in that calendar year can produce significant state tax savings.

The critical planning caveat: the residency must be genuine and complete before the event occurs, and the day count for that calendar year must be clean. A large liquidity event that occurs in the same year you "move" to Florida, while you are still spending significant time in New York, is precisely the scenario that triggers a New York residency audit. Get qualified tax counsel involved well before the event — not after.

Still Owning Property in NY/NJ After the Move

Many Naples buyers keep their northeastern home for a period after establishing Florida residency — renting it, using it seasonally, or simply not yet ready to sell. This is common and manageable, but it introduces specific complications that need to be understood and planned for.

Maintaining a "permanent place of abode" in New York — which your old home almost certainly qualifies as — is one of the two conditions for New York statutory residency. If you also spend 183 days or more in New York, you may owe New York income tax regardless of your Florida domicile. The risk is real for people who are genuinely transitioning — spending winters in Naples but still returning to New York for extended periods during the rest of the year.

Rental income from the northeastern property is sourced income — it is taxable in New York or New Jersey regardless of your residency. If the property is rented, you will likely need to continue filing state returns in the old state to report that income. The elimination of New York income tax applies to Florida-sourced income; it does not eliminate your obligation to pay New York tax on New York-sourced income.

From a financial planning perspective: the sooner you simplify your property ownership to Florida only, the cleaner your tax situation becomes. Holding property in both states indefinitely creates ongoing audit risk, ongoing filing obligations, and ongoing complexity that typically costs more in professional fees than the holding benefit is worth.

Estate and Inheritance Tax — Florida's Clean Position

Florida has no state estate tax and no state inheritance tax. This is a significant planning advantage for high-net-worth households who have been navigating New York's estate tax structure, which applies at a lower exemption threshold than the federal estate tax and includes a "cliff" provision that can create substantial tax liability if the estate exceeds the exemption by a small amount.

New Jersey eliminated its estate tax in 2018 but retains an inheritance tax that applies to assets transferred to certain classes of beneficiaries — siblings, nieces, nephews, friends — at rates up to 16%. For New Jersey residents with complex family structures or charitable intentions, Florida's clean position on both taxes is meaningful.

One complication: if you own real property in New York or New Jersey at the time of death, that property may still be subject to the estate and inheritance laws of those states regardless of where you resided. Simplifying property ownership to Florida before death — or using appropriate planning structures — is another reason the "keep the old house" strategy has long-term costs that are not always immediately visible.

What Florida Costs More — The Honest Offset

Florida's income tax advantage is partially offset by higher costs in specific categories that northeastern buyers do not always anticipate. None of these eliminate the tax benefit — but they belong in the full financial picture.

- Homeowners insurance: Florida insurance premiums are significantly higher than northeastern equivalents, particularly for coastal properties, properties with older roofs, or properties in flood zones. A $500/year homeowners premium in New Jersey can become $8,000–$15,000/year in Naples depending on the property.

- Flood insurance: standard homeowners insurance does not cover flood damage. Properties in FEMA-designated flood zones require separate flood coverage. Even voluntary flood coverage is advisable for some Naples locations not technically in a required zone.

- HOA and CDD fees: most Naples communities have HOA fees. Many newer communities also have CDD fees — an annual infrastructure assessment that appears on the property tax bill and does not go away when the CDD bond is paid off (though the amount changes). These are recurring carrying costs that do not exist in most northeastern neighborhoods.

- Sales tax on large purchases: Florida's sales tax of 6% plus Collier County's 1% surtax applies to most goods. When furnishing a new Naples home or making major purchases in year one, this cost is noticeably higher than in states with lower or more exemption-heavy sales tax structures.

Compare your full cost of living before and after moving from the Northeast to Naples — taxes, housing, HOA, insurance, and more.

Open CalculatorScott walks buyers through the complete Naples cost picture — not just the purchase price. Free, no obligation, 35 years in the market.

Talk to Scott